Don't get ripped off when storm chasers blow into town to repair roofs and broken windows. Here's what you need to know about storm damage, homeowners insurance, and finding a good repair contractor.

What To Do After Hail Damages Your Roof

Hail and wind damage account for the most common homeowners insurance claims, totaling 38 percent of all claims, according to data from the Insurance Information Institute. Wind and hail damage claims also include damage caused by hurricanes and tornados.

A wind and hail damage claim ranks as the fourth most expensive claim with an average cost of $10,182 per claim, based on information collected by the III. So what should you do when roofing contractors come knocking?

What to Do Following Storm Damage

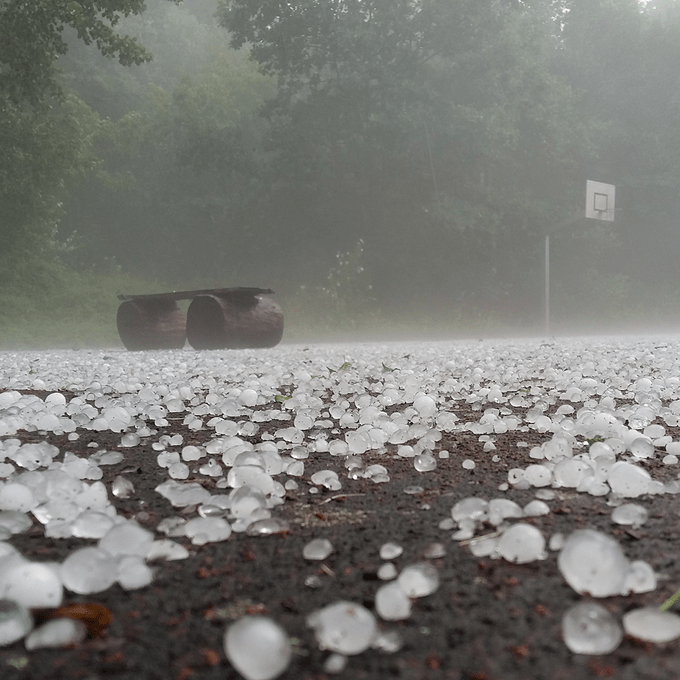

It’s tough to know what’s worse, the storm damage itself or what follows after. Many of you have gone through it—hunkered in the basement hoping a tornado doesn’t drop when all of a sudden you hear something that sounds like golf balls slamming into your house. But you don’t live near a golf course. Is your car outside? How is the roof holding up? Did a tree just snap? Was that breaking glass?

When the last wave of awful weather finally passes and you’re out inspecting the damage, the first wave of storm-chasers starts to hit. In some cases, they are knocking on your door before the last raindrops have stopped. They have been driving around, listening to the radio, and getting hail reports sent to their phone. They have been cheering for the largest hail possible and this could be the storm they have been waiting for! Here’s what to look for and what to avoid in the multi-billion dollar game that is storm damage restoration.

Knock, Knock!

First of all, just because a company knocks on your door does not mean that they are a bad company. Local companies that got fed up with losing business to out-of-towners have jumped into door-knocking as well, even if it isn’t part of their normal operations. The important thing to remember is that you should NEVER sign anything until you’ve done your homework. Many companies that do primarily storm damage follow storms around the country, so you want to make sure that someone will be around to service your roof if starts to leak or if any other problem pops up.

How Storm Damage Contractors Operate

The process is this:

- After a storm you’ll get a knock on your door by someone offering to do a free inspection on your roof. This sounds pretty good to you since you don’t know exactly what hail damage on a roof looks like.

- When they come back down, they’ll tell you that there is damage up there and that he/she happens to be an expert when it comes to working with insurance adjusters.

- They will then take out an insurance commit form and explain what it means. They say that this form gives them permission to work on your behalf with your insurance adjuster. By signing it, you agree that if the damage gets covered, this is the company you will use. If it doesn’t get approved, then you aren’t committed to anything.

This seems like a reasonable request to you since they were nice enough to go up and do a thorough examination of your roof. And after all, there is no money out of your pocket besides the deductible— so why not?

Here’s why not. The company is headquartered out of state, and when this storm is tapped out they are moving on to the next one. Choosing a storm damage contractor should be no different than choosing a contractor for anything else. Use a local company with longevity who will be around to help if anything needs fixing. Examine the contractor’s labor or “workmanship” warranty. Read reviews and check out the BBB. Go and take a look at the jobs they have done. Who you hire to fix your roof is too important of a decision to just sign with the first person that knocks on your door, but you would be surprised at how many people do.

Know the Parent Company

Over the years, more and more homeowners have started to ask if the company is local, so the storm-chasers have adjusted. Some out-of-state companies will come in and set up shop with a local company and do business under that company’s name. The local company gets a cut and will be here to do the service if needed. When the person who knocks on your door has a southern accent but is “working” for a company that has been in Minnesota for 20 years, that just might be the case. There is also the possibility that it’s a Minnesota company that does work nationally, and they bring in all the resources from around the country when the big one hits here. The way to find out is to ask more questions and do your research.

Are You Signing a Permission Slip or a Contract?

Some salespeople are deceptive when it comes to getting that original signature. They will tell you it is just for permission to talk to your insurance company, but they will gloss over the part where it says you must do the work with them. My best advice would be to ask them to leave behind their form so you can look it over. If they are not willing to do this, send them on their way. The second option is to avoid all door-knockers and simply call the company you would like to inspect your roof so YOU are in control of making this important decision.

What About Replacing Windows After a Storm?

Another important question to ask any contractor is if they will handle damaged windows in your insurance claim. Many are up for the quick score of roofing or siding, so they ignore damage to the windows. Windows are more work to identify, take more time to order for custom-sizing (thus delaying the final payment), and for many contractors, it is not their expertise. If you have aluminum-clad windows, make sure to have them inspected. In some storms, the hail and wind are so severe that the seals of the double pane windows fail. This results in a cloudy look to your windows that you can’t get clean, sometimes with visible condensation between the two panes. Make sure everything is looked at during the inspection.

While insurance companies have their roofing and siding prices fairly locked in, they really don’t have a clue on where to price windows since there are so many brands/styles. This usually takes a quote from the contractor and some back and forth to lock in on a price that both the contractor and the insurance company can agree on.

Contractor vs. Adjuster

One last thing to remember is that many of these storm-chasing contractors will tell you that you have damage even if you don’t. They are simply playing the odds that maybe one of the adjusters who comes out might be new and could be talked into approving the job. The insurance adjusters usually know who these companies are and shake their heads when they see who you signed with. If the adjuster does not approve the job, the contractor may ask you to threaten the insurance company with losing your business if they don’t approve it, and things can get ugly from there.

There are many battles between adjusters and contractors, and many times they play out right in front of the customer. If you see this happening, have the contractor show you what damage they are seeing. Have them take pictures of it if you don’t feel like getting up on your roof. There are certainly times when the contractor is right and the insurance company is not being fair about obvious damage. Just be aware that some contractors practice the “every house has damage” angle.

What to Know About Insurance Following a Storm

Now that you know some of the things contractors may try to pull, be aware that the insurance companies have their moments as well. Sometimes your agent tries to talk you out of making a claim. Sometimes they low-ball the estimate and the contractors have to work hard for supplements that are needed just to make the job turn a profit (getting multiple quotes would let you know pretty quick if your insurance company is overpaying or underpaying). Sometimes their first adjuster doesn’t cover obvious damage, and it takes the contractor to schedule a re-adjustment to get the repair to go through. Sometimes they change the terms of your coverage without you knowing it.

Pay Attention to Home Insurance Policy Changes

Some states require full house replacement for siding or roofing if some product is damaged and the product is no longer made by the manufacturer. However, some companies will hide a change in the 20-plus page document they send each year which states that is no longer valid unless you add a low-cost rider to your coverage. Most people would pay the small extra charge to cover this, but they don’t even know that it has changed. When you receive that booklet, call your agent and ask if anything is changing that you should know about (or take the time to read the whole boring thing). Otherwise, you may be in a situation where you have to find the “closest match available” for only the siding or roofing that is damaged. This could mean a checkerboard look to your house as your insurance company only covers individual shingles or siding panels. Winter damages home every year. Be prepared for the next storm by knowing which parts of your home are most susceptible to winter storm damage.

What to Know About Roof Replacement Warranties

Also, good luck finding a contractor who will put a warranty on a roof that they are only doing part of. No contractor wants to be held responsible for a leak in part of the roof they didn’t do. Feel free to call your agent and go through these questions about your individual policy.

We all know there will be storms every summer. If the big one hits your area, take some time before making any decisions and try to resist the multiple door-knocks. Or you can do what a neighbor of mine did … he put a sign by his door that said, “Please leave your fliers here!” Underneath was an arrow pointing to his garbage can.

This is a guest blog post by Ryan Carey of My 3 Quotes and originally appeared at Structure Tech

Also, learn how much does hail damage impact a car’s value.